14+ Sample Debt Demand Letters

-

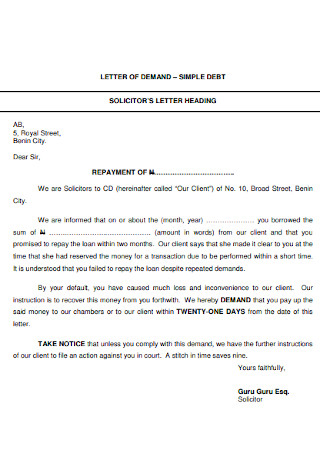

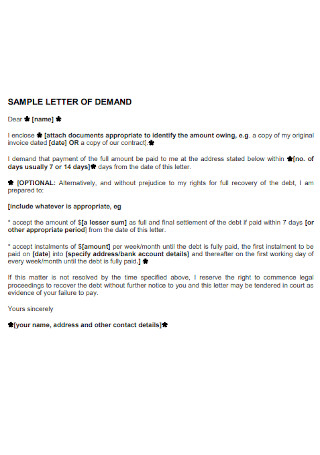

Simple Debt Demand Letter

download now -

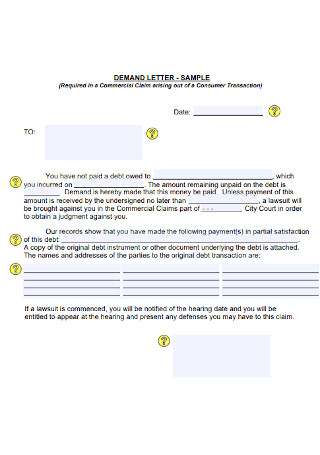

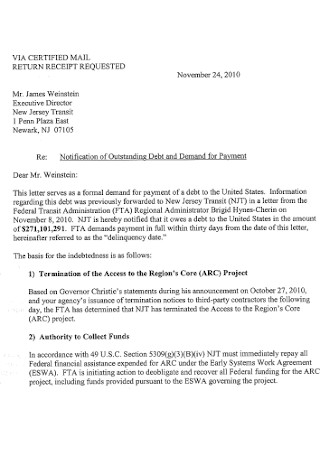

Sample Debt Demand Letter

download now -

Debt HR Demand Letter

download now -

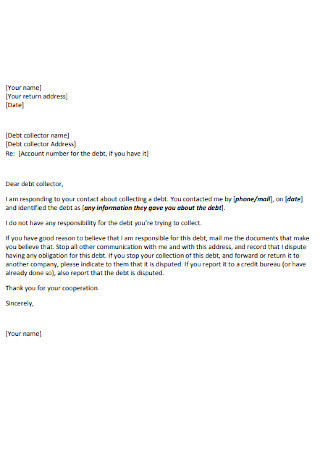

Debt Collector Demand Letter

download now -

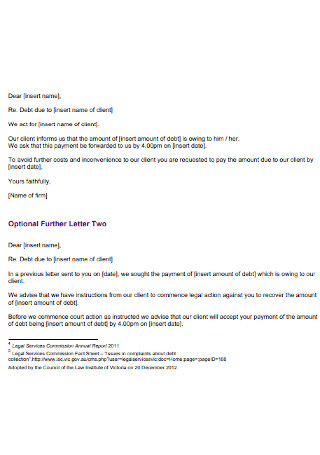

Debt First Demand Payment Letter

download now -

Debt Legal Services Demand Letter

download now -

Debt Recovery Letter of Demand

download now -

Debt Demand Payment Letter

download now -

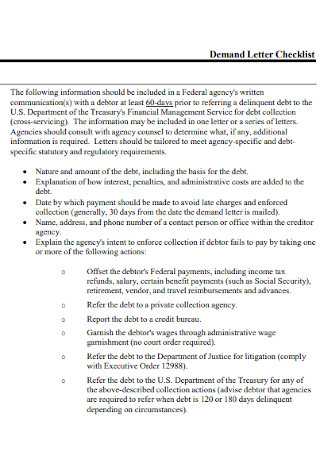

Debt Demand Letter Cheklis

download now -

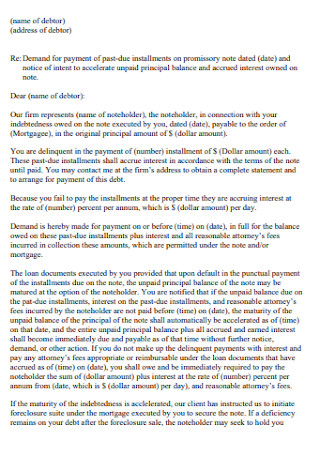

Basic Debt Demand Letter Template

download now -

Formal Debt Demand Letter

download now -

Debt Seven-Day Demand Letter

download now -

Sample Debt Demand Letter Example

download now -

Debt Recruitment Demand Letter

download now -

Company Debt Demand Letter

download now

FREE Debt Demand Letter s to Download

14+ Sample Debt Demand Letters

What Is a Demand Letter?

Benefits of Demand Letters

Types of Debt

Tips for Writing an Effective Demand Letter

How to Avoid Debt

FAQs

How long does settlement take after a demand letter?

What occurs following a demand letter?

Can you ignore a demand letter?

What Is a Demand Letter?

A demand letter is a formal document one party sends to another to settle a dispute. To right a wrong or resolve a dispute, the sending party may issue a demand for payment or another action. The recipient may be in financial dereliction, have violated the terms of a contract, or have failed to fulfill an obligation. Typically, they are written by attorneys. Demand letters are the initial move aggrieved parties take before initiating legal action against the recipient. In most situations, a demand letter is sent as a courtesy or a reminder after all other failed attempts before a legal action plan is taken. It is typically sent via certified mail, giving the recipient one last opportunity to rectify the situation, whether financial or otherwise. Most demand letters contain instructions for resolving the issue, including payment information and due dates.

Benefits of Demand Letters

In demand letters, the details of a dispute and the disputed issue(s) are outlined. They clarify the situation so that all parties can comprehend it. The demand can then specify the resolution the originator desires, such as monetary compensation or accommodations. A demand letter can also provide notice that legal action will be pursued if the sender’s demands are not met. As a result, the recipient of a well-written demand letter may now be more inclined to negotiate in good faith with the submitter, given the gravity of the situation. Disputes are frequently prolonged when one party is unresponsive or flatly refuses to negotiate. In these circumstances, a formal demand letter can explain that legal action is possible if settlement discussions are not initiated immediately, openly, and honestly. In addition, demand letters provide basic and specific information regarding the sender’s request and its reason. Such precision aids in the avoidance of misunderstandings and miscommunications and expedites the settlement of credit dispute letters.

Types of Debt

There are numerous types of debt, each with its purposes and requirements. When students obtain federal student loans to pay for college, they receive a certain amount of money they commit to repaying with interest. Students now have access to a variety of repayment options. If they select the standard payment plan, they must make fixed monthly payments for ten years, at which point their debt will be repaid entirely. These monthly payments will represent a component of the debt’s principal and the accrued interest. The majority of debt falls into at least one of the following categories:

Tips for Writing an Effective Demand Letter

Writing an effective letter of demand is crucial in nearly every civil case. It introduces you and your client to the opposing party’s representative, who could be an attorney, an insurance adjuster, or a risk management action plan. This initial impression will reveal much about how they should evaluate you, your client, and the case you represent. In addition, the letter establishes the tone of settlement negotiations. As the cost of trying a case increases substantially and fewer cases go to trial, more cases are settled before trial. Therefore, placing your client in a strong negotiating position is essential. Here are some guidelines to assist you:

1. Be Organized

You should collect all relevant documents at the beginning of your client’s case. In a personal injury case, this may involve submitting requests for copies of your client’s medical and employment records, obtaining police reports, and gathering important business documents the client may possess. This may include a copy of the contract and any correspondence between the parties in a contract case. The core of the issue will dictate the required documentation. Writing an effective demand letter will be possible with a complete information sheet templates, so obtaining copies of documents as soon as feasible is essential.

2. Submit the Letter Without Delay

It is crucial to submit the demand letter promptly, i.e., as soon as possible, for the above reasons. It will demonstrate that you control the situation and aid the adjuster in establishing reserves. If your letter is being held up because you are awaiting documentation, inform the adjuster so they can make the appropriate notation in their file. In addition, as stated in section 1, if your case requires prolonged treatment, provide periodic updates and indicate that additional information will be provided as it becomes available.

3. Include Claims-Related Information in All Correspondence

Before submitting the demand letter, you should have sent the opposing party a note of representation containing your client’s signature. If applicable, the opposing party will then send a confirmation letter, including their claim or file number and policy number. Please include the following information in the reference section of all your correspondence: your client’s name, their client’s name, the date of the incident, the claim number, and the policy number, as applicable. Include the case name, the county where the lawsuit was submitted, and the court case number if a lawsuit has already been filed. You want to make it as simple as possible for attorneys, adjusters, and insurance companies to route your correspondence to the correct individual.

4. Use Subheadings

Utilizing subheadings within the body of the demand letter will facilitate the reader’s navigation of each topic. Subheading titles can be modified based on the nature of the case and the number of damages sustained. Also, it is recommended to include precise details, particularly regarding the summary of facts, medical treatment, and general damages. Having specific points will aid the adjuster in evaluating the case accurately. Refer to the document containing the truth, which should be affixed as an exhibit, along with its number or letter. General damages are complicated to quantify, but by delineating your client’s obstacles, you can make the abstract concept of pain and suffer more tangible.

5. Provide a Deadline for Response

At the end of the note, you should say something like, “This offer will be open for 30 days,” so that the other person knows when they have to decide. Many people say you should also include text saying you’ll sue if the case doesn’t settle, but that’s unnecessary. When the adjuster or lawyer reads the demand letter, they will know that a complaint will probably be made if the case doesn’t settle.

How to Avoid Debt

Debt can potentially harm your financial well-being, but it need not be the enemy. If you incur debt for a worthwhile purpose, and if paying it back works comfortably within your budget, debt can assist you in developing sound financial habits, enhancing your credit, and achieving your objectives. However, there are circumstances in which it is preferable to avoid debt. For instance, credit card debt for which you can only afford the minimum monthly payment can result in sky-high interest rates and lower credit scores. These steps can help you remain on the right side of debt, which means only incurring debt when it is necessary, affordable, and beneficial.

1. Create a Reserve Fund

It may seem contradictory, but an emergency fund is a crucial component of debt avoidance. Specialists suggest saving three to six months’ worth of essential expenditures, or more, if your work is seasonal, freelance work agreement, or unpredictable, in case you lose your job. An emergency fund can also cover unexpected expenses that would otherwise be charged to a credit card. Use your emergency fund to pay for your car repairs or dental work, for example, if you need them immediately. This way, you won’t abruptly incur credit card debt that could take years to pay off.

2. Choose a Budget Plan

If you consistently make purchases you cannot pay off at the end of each month, overwhelming credit card debt can creep up on you. Creating a budget plan for each dollar you earn is the best method to avoid overspending. A budget can be as general or as specific as necessary. It may involve separating your spending into necessities, wants, and short- and long-term financial objectives.

3. Stick to a Savings Routine

Automating your savings plan simplifies creating an emergency fund and saving for other goals, such as retirement. Additionally, separating this money from your checking account makes you less likely to spend it and incur debt.

4. Pay Your Monthly Credit Card Balance in Full

Credit cards invite you to purchase expensive items you cannot immediately afford, given that you can pay off the balance in installments. Only buy things for which you will have sufficient funds in your checking account by the due date. You will never incur interest charges, and your credit utilization will remain low, potentially boosting your credit score. Moreover, you will not incur debt that may be difficult to eliminate.

5. Only Borrow What Is Necessary

When seeking other forms of credit, such as a car loan, mortgage, student loan, or personal loan, choose the smallest loan to help you achieve your objectives. A substantial down payment on a vehicle or mortgage can reduce your monthly payments. Mainly, student loans should be considered a last resort for college after federal, state, and school grants, private scholarships, and work-study funds have been exhausted.

FAQs

How long does settlement take after a demand letter?

After sending a demand letter, there is typically no predetermined time limit to settle. The shipper provides a deadline to the recipient. This is the expected response time from the recipient. After the initial demand letter has been sent, both parties can convene to reach an agreement and resolve the dispute.

What occurs following a demand letter?

After sending a demand letter, the correspondent awaits a response. The recipient has the opportunity to review the letter and its contents, as well as confirm all the facts. The recipient may then respond with a counteroffer, a settlement, or a refusal to oblige with a list of reasons. The recipient may employ an attorney to compose their demand letter.

Can you ignore a demand letter?

Some individuals may choose to disregard a demand letter for various reasons. But doing so is not in your best interest. If you ignore the letter and the matter proceeds to court, you must explain to a judge why you did not respond to the sender’s good-faith effort to settle.

Numerous advantages are associated with the use of demand letters to resolve disputes. If a demand letter is unsuccessful, the only recourse may be to initiate the appropriate legal proceedings. An employment and human rights attorney can assist in drafting a demand letter that is as persuasive and effective as possible, as well as offer guidance on the following measures to take if this does not produce the desired result.