12+ SAMPLE Income Statement and Balance Sheet

-

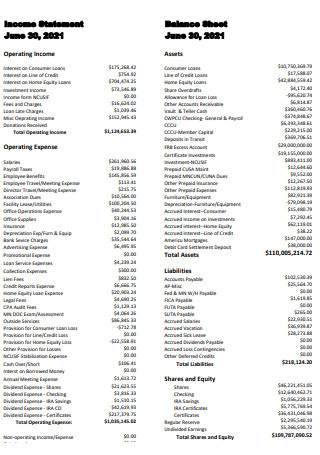

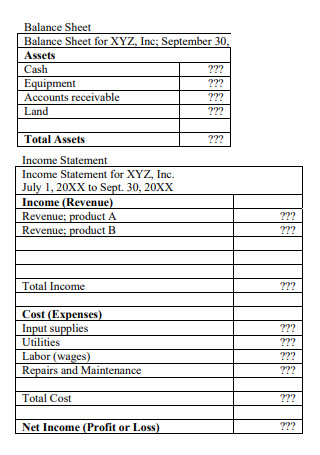

Basic Income Statement And Balance Sheet

download now -

Income Statement And Balance Sheet Example

download now -

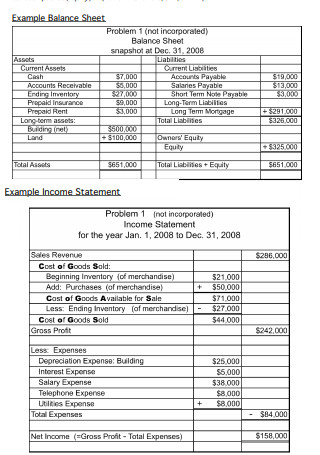

Relationship Between Income Statement And Balance Sheet

download now -

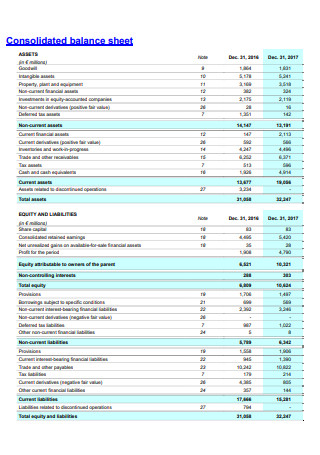

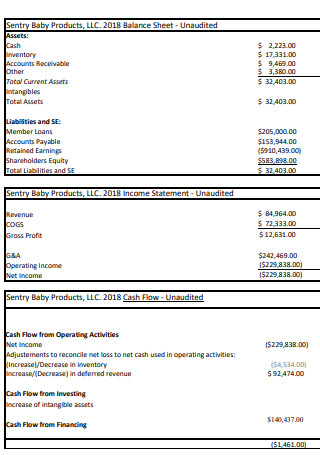

Consolidated Balance Sheet

download now -

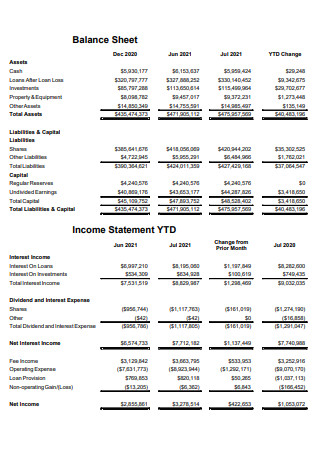

Income Statement And Balance Sheet

download now -

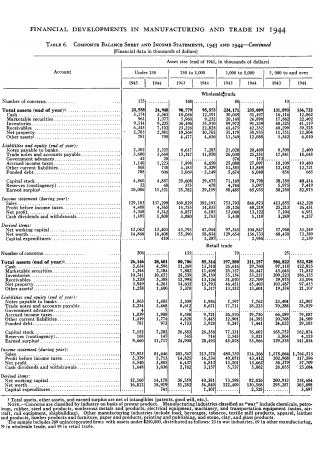

Composite Balance Sheet and Income Statements

download now -

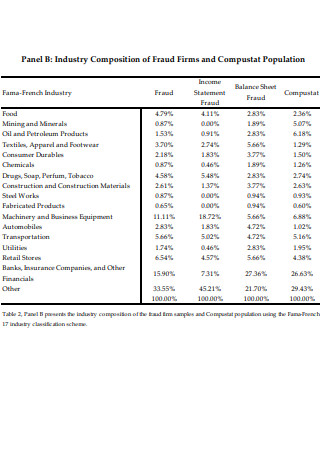

Income Statement Fraud and Balance Sheet Fraud

download now -

Formal Income Statement and Balance Sheet

download now -

Personal Income Statement and Balance Sheet

download now -

Financial Position of Income Statement and Balance Sheet

download now -

Potential Indicators of Income Statement and Balance Sheet

download now -

First Quarter Income Statement and Balance Sheet

download now -

Power Development Board Income Statement and Balance Sheet

download now

FREE Income Statement and Balance Sheet s to Download

12+ SAMPLE Income Statement and Balance Sheet

What Is an Income Statement and Balance Sheet?

Tips to Augment Income

Key Concepts Related to Balance Sheets and Income Statements

How to Create an Income Statement and Balance Sheet

FAQs

What is the difference between a balance sheet and an income statement?

How is the income statement related to the balance sheet?

What is an income statement and balance sheet explained with examples?

What Is an Income Statement and Balance Sheet?

An income statement and balance sheet are essential financial documents. Income statements are typically used to measure revenue, cost and expenses. Balance sheets, on the other hand, help determine an individual or organization’s financial standing or health.

According to data published on Statista, the United States’ Federal Reserve had $7.17 trillion worth of assets on their balance sheet as of June 2020.

Tips to Augment Income

An ideal situation would be where one’s income can meet or match one’s expenses. Unfortunately, the reality is that a lot of people are unable to meet their needs because of a lack of income. Or in some cases, their expenses and lifestyle choices significantly exceed their income. There can be several ways to augment or supplement one’s income. It may not be easy at times, but if done correctly and responsibly, you can earn a little extra.

Key Concepts Related to Balance Sheets and Income Statements

When it comes to balance sheets and income statements, there are a number of key concepts that you must familiarize yourself with first. You cannot craft a sound or accurate balance sheet or statement without knowing the basic components that comprise it. The following examples describe just some of these main concepts needed in creating an income statement or balance sheet.

How to Create an Income Statement and Balance Sheet

To create an income statement and balance sheet, you need to have a firm grasp on your financials. And if you are looking for a quick and easy way to create one, using a ready-made template can save you a lot of time and energy. Easily download a sample template of your choice and input the right data. Follow the step-by-step tutorial below to get started.

Step 1: Format

Before inputting any financial data or records, you need to establish a structured format. It is important to choose a format that you can work with and one that will serve your specific needs as well. Fortunately, there are dozens of predesigned statements and spreadsheets that are available to download and edit. Income statements and balance sheets are typically created using applications such as Microsoft Excel or Google Sheets. What’s important is how well you present and arrange the data. You not only have to make sure the format is clear and comprehensible, but it should also be flexible or easy enough to modify.

Step 2: Numbers

The next step is to input the numbers or financial data. Anyone can create a basic income statement or balance sheet. Individuals may feel the need to make one to help get their finances in order. It is even more common for companies and establishments to require these for their financial requirements and monitoring. As mentioned in the previous section, important items such as assets, liabilities, expenses, and revenue need to be incorporated in your statement or spreadsheet. But this will still highly depend on your individual or organizational needs. Lastly, make sure the amounts you input are accurate and updated.

Step 3: Review

Once you have inputted the financial amounts, you need to ensure that your data is true and correct. Like for any important document, it is important to review all data before finalizing and submitting it. Reviewing is an important step that should not be overlooked. It can be easy to dismiss or skip this step especially if it’s inconvenient or if you are short on time. A balance sheet can have a staggering amount of numbers and figures. And in accounting, even just one mistake can upend the entire spreadsheet. Make sure to review your income statement and balance sheet once it’s completed. Better yet, have a colleague or trusted friend review it a second time too.

Step 4: Next Steps

Lastly, the work does not necessarily end once you have finished the last spreadsheet. Yes, the numbers and data are crucial. But it is also important to remember that more than the data itself, it is what you do with the information you have gathered and how you apply it. The last step is to come up with recommendations or a plan based on the data you just inputted. What are your next steps? If your overall conclusion is that your financial standing is unfavorable or it needs significant improvement, then you need to act or plan accordingly.

FAQs

What is the difference between a balance sheet and an income statement?

An income statement is mainly and exclusively focused on income, revenue, cost and expenses. But a balance sheet is more general in a sense that it can contain several financial data. It usually also includes assets and liabilities.

How is the income statement related to the balance sheet?

Since you need to create a balance sheet to determine your financial standing, you would need to consider your income and expenditures. An income statement, therefore, can be directly linked or integrated into a balance sheet.

What is an income statement and balance sheet explained with examples?

As mentioned all throughout the article, an income statement and balance sheet are both financial documents that are usually used to determine one’s financial standing or financial health. Browse the selection of example templates above to get a more concrete picture of what balance sheets and income statements are.

To better track or monitor your finances, you need to know how to create an accurate income statement and balance sheet. Browse the wide collection of editable templates above to get started on your own statement or sheet today!